COMMERCIAL MORTGAGES

What is a Commercial Mortgage

A commercial mortgage is a loan given to an individual or business entity to purchase, develop or refinance a commercial property. It’s an essential financial facility that can help you expand and grow your business, allowing you to take advantage of lucrative property opportunities. Obtaining a commercial mortgage can be a straightforward and efficient process with the correct information and guidance.

To add more context to our summary, a commercial mortgage is a loan used to purchase or refinance a business property, such as an office building, retail store, or apartment building. The borrower will use the loan to pay for the purchase of the land and buildings.

A commercial mortgage is secured against the purchased property and can be used to finance a wide range of projects, from the owner-occupied property, to small business investments and large-scale development projects.

Who Can Obtain a Commercial Mortgage?

Generally, commercial mortgages can be obtained by business owners and investors interested in purchasing a commercial property. However, they can also be obtained by individuals or companies looking to refinance an existing commercial mortgage.

To qualify for a commercial mortgage, borrowers must typically have a good credit score and demonstrate the ability to make regular payments on the loan. Additionally, lenders may require borrowers to provide financial statements and other forms of income verification.

Commercial Mortgage Criteria

Commercial mortgage criteria vary depending on the lender. Generally, for a commercial mortgage loan to be approved, you must provide documents such as tax returns, business financial statements, and business plans.

Lenders may also require additional collateral or personal guarantees from property owners. In addition, lenders may consider factors such as credit scores, debt-to-income ratios, and experience in property or business.

To ensure your application is approved, ensure you have all the necessary documentation to prove that you can repay the loan. It would be best if you also were prepared to provide details on how you plan to use the commercial mortgage funds.

Here are the commercial mortgage criteria in a list

- Tax Returns

- Business financial statements

- Business plans

- Collateral or personal guarantees from owners of the property

- Credit scores

- Debt-to-income ratios

- Experience in real estate

- Detailed plan for how funds will be used

- Proof of ability to repay the loan

Any other documents or evidence deemed necessary by the lender

What we offer

Business loans

Bridging Loan From £50K- £50M

Bridging Loan From £50K- £50M

What are Business Loans?

Business loans are funds provided by financial institutions, such as banks and other lenders, to business owners. They can provide the capital needed to start or expand businesses.

Generally, business loans come in two forms: secured and unsecured. Secured business loans require collateral, typically an asset owned

What are Business Loans?

Business loans are funds provided by financial institutions, such as banks and other lenders, to business owners. They can provide the capital needed to start or expand businesses.

Generally, business loans come in two forms: secured and unsecured. Secured business loans require collateral, typically an asset owned by the business, to guarantee the loan.

Conversely, unsecured business loans do not need collateral. Before applying for financing, business owners should understand the differences between secured and unsecured loans.

Business owners can use loans for various reasons, such as hiring new employees, purchasing equipment or inventory, expanding operations, or starting a business.

Moreover, business loans help with cash flow management, enabling quick and easy access to funds. The purpose of business loans is to provide necessary funds while minimising the financial risk involved in borrowing money.

Types of Business Loans

When business owners are looking for business loans, they have several options. Each business loan type has different requirements and offers unique benefits to business owners. We are going to explain some of the most common business loan types below:

1. Small Business Loans

Small business loans are a great option for owners needing capital to expand their operations. They provide access to funds not available through traditional lending sources, such as banks and credit unions. Small business loans are typically easier to obtain and come with more flexible terms than other financing forms. The benefits include lower interest rates, longer repayment periods, and more lenient credit requirements.

However, business owners should carefully consider the terms and conditions before applying to ensure suitable financing. With the right loan, small businesses can grow and thrive. Additionally, owners need to understand the application process.

They should ensure all paperwork is in order before submitting a loan request for quick processing. Small businesses will also need to provide proof of financial stability and any required collateral. Once approved for a small business loan, borrowers must adhere to specific repayment terms established with the lender

. 2. Start-up Business Loans

Start-up business loans are a great option for entrepreneurs needing capital to start their businesses. These loans provide access to funds unavailable through traditional lending sources, such as banks or credit unions. Moreover, start-up business loans usually have more flexible terms than other small business financing. They often feature lower interest rates and longer repayment periods. Additionally, start-up business loans tend to have more lenient credit requirements than other small business financing options.

When applying for a start-up business loan, it is important to consider all aspects of the loan carefully. Business owners should pay special attention to the lender’s terms and conditions.

They must ensure they understand them fully before agreeing to anything. Additionally, it is important to provide all necessary paperwork to the lender.

This includes proof of financial stability and any required collateral. Once approved, entrepreneurs should maintain their repayment plan to stay in good standing with the lender.

Overall, start-up business loans can give small businesses the capital needed to start operations quickly. With proper research and consideration of all terms and conditions, small businesses can benefit from this financing opportunity.

3. Short Term Business Loans

Short-term business loans are a great way for businesses to access extra funds quickly. They don’t require waiting months for approval.

Furthermore, they can be used for various purposes like purchasing new equipment or expanding operations. These loans typically require less paperwork and have shorter repayment periods than other financing types.

Additionally, they often have lower interest rates and fees, making them attractive for covering short-term expenses or growth. Businesses should consider all options before choosing a loan that best meets their needs. However, short-term business loans can be an excellent choice when time is crucial.

For those considering a short-term business loan, it’s important to understand the loan details before signing. It’s also essential to shop around for the best rates and terms that suit your business. With careful planning and research, a short-term business loan can ensure your organisation’s success.

In essence, short-term business loans are an excellent option for businesses needing extra funds quickly. They are suitable for those lacking resources for traditional bank loans. Knowing when to use one could be a wise decision for any small business owner.

4. Long Term Business Loans

Long-term business loans are an excellent way to finance business growth. These loans are generally larger than short-term loans. They often require collateral, like real estate or equipment. Additionally, long-term loans usually have lower interest rates. They also offer flexible repayment plans that suit a business’s life cycle.

Depending on the loan size and lender type, long-term financing options vary. These can include traditional bank loans, SBA lending programmes, or venture capital investments. Specialised financial products are also available. Access to these funds helps businesses expand operations and purchase inventory.

Moreover, it enables making important investments in future success. A well-structured long-term loan can elevate your company to new heights!

5. Secured Business Loans

Secured business loans suit businesses needing large loans and capable of providing security. This type of loan uses assets such as property, equipment, or stocks and shares as collateral.

Consequently, the lender can seize these assets if the borrower defaults on the loan.

Furthermore, secured business loans typically offer better terms than unsecured loans. These include lower interest rates, longer repayment periods, and larger loan amounts. To apply, you must provide evidence of assets to use as collateral. The lender might also have additional requirements before approving the loan.

Once approved, you can use the loan for various business activities. These activities include expansion, purchasing products, or marketing campaigns. However, failing to repay could lead to losing the collateral. Thus, ensure you can confidently meet repayments.

A secured business loan can effectively help a business achieve long-term goals. Therefore, if considering a secured business loan, evaluate all aspects carefully. With proper planning and financial management, these loans can benefit businesses seeking larger funds with better terms.

6. Unsecured Business Loans

Unsecured business loans offer various financing options for small businesses without needing collateral. These loans provide much-needed capital to help expand businesses, allowing owners to maintain their assets.

Moreover, unsecured business loans can be used for various purposes, such as equipment purchases or expanding operations. They also support hiring additional staff or launching a new product. Additionally, they can cover short-term cash flow needs, like purchasing inventory or paying rent and bills.

When applying for an unsecured business loan, having a good credit score and demonstrating sound financial management is crucial. With the right lender and terms, unsecured business loans can be an invaluable tool for business growth and success.

7. Government Business Loans

Government business loans are a great way for businesses to access funding and start or expand their operations. These loans provide long-term financing at low-interest rates, helping entrepreneurs get needed resources to grow.

Furthermore, they may include grants, tax credits, and other forms of assistance. Typically, federal, state, and local organisations, like the Small Business Administration (SBA), allocate these loans.

To qualify for a loan, businesses must meet certain criteria, such as having a solid business plan, adequate collateral, and strong financials. Additionally, businesses need to demonstrate how they will use the funds to be approved. Government business loans can help entrepreneurs achieve their goals and create successful businesses.

Consequently, companies can start new projects, purchase equipment, hire staff, and invest in marketing to increase their customer base. Moreover, government business loans may provide access to additional resources like business counselling and training programs. Getting approved for a loan is the first step towards achieving success with a small business.

8. Business Bounce Back Loan

The UK Government’s Business Bounce Back Loan scheme supported small and medium-sized businesses affected by the Coronavirus pandemic. This loan allowed businesses access to up to £50,000 in funding, with a repayment period of 6 years.

Initially, the loan is interest-free for the first 12 months, then carries an interest rate of 2.5%. The Government guaranteed up to 80% of the loan, so no personal guarantees were required from business owners.

Additionally, the Business Bounce Back Loan could be used for any legitimate business purpose, including covering lost revenue, maintaining cashflow, and financing capital investments. It was designed to help businesses overcome short-term financial difficulties due to the Coronavirus pandemic.

Furthermore, applications for the Business Bounce Back Loan were available through accredited lenders and banks. Businesses needed to provide evidence of their turnover, as well as other financial information. To qualify, businesses must have been trading before 1st March 2020 and affected by the Coronavirus pandemic.

The Business Bounce Back Loan offered a lifeline for businesses whose trade decreased because of the pandemic and struggled to stay afloat. This loan provided much-needed financial stability, allowing them to survive and thrive in the future. The government may reintroduce this type of loan in similar future circumstances.

9. Personal Business Loans

Personal business loans help entrepreneurs and small businesses get funds to start, grow, or expand operations. These loans are generally issued by banks, credit unions, and other financial institutions.

Lenders require borrowers to have good or excellent credit scores before approving a loan. Since terms and conditions vary greatly by lender, it is crucial to shop around for a suitable loan.

These loans can provide working capital or finance equipment purchases. Additionally, they may refinance existing debt or help purchase real estate.

With flexible repayment options and competitive interest rates, personal business loans can effectively support your business.

Comparing a Business Loan vs. Personal Loan

Business loans and personal loans differ in several ways. A business loan is specifically designed to meet the needs of a business, whereas a personal loan is typically for individual use.

Business Loans:

- Purpose: Specifically designed to meet the needs of a business

- Type: Typically secured/unsecured loans

- Term: Longer repayment terms

- Repayment: Repayment amount remains relatively consistent throughout the loan term

- Interest Rates: Generally lower interest rates than with personal loans

Personal Loans:

- Purpose: Typically for individual use

- Type: Unsecured loans

- Term: Shorter repayment terms

- Repayment: Repayment amount increases as the loan term progresses

- Interest Rates: Generally higher interest rates than with business loans

How to Get a Business Loan

Obtaining a business loan can be difficult. However, it is essential for businesses aiming to grow and expand operations.

Firstly, create a detailed business plan outlining the loan’s purpose, such as expanding operations or buying equipment.

Next, the applicant must show their ability to repay the loan. They should provide financial documents like bank statements, credit reports, and tax returns.

Additionally, businesses must shop for the ideal rate and lender that fits their needs. This step is crucial before committing to a loan agreement.

Following these steps can help companies secure the funds they need to succeed.

Bridging Loan From £50K- £50M

Bridging Loan From £50K- £50M

Bridging Loan From £50K- £50M

What is a Bridging Loan?

A bridging loan is a short-term financing option that helps borrowers bridge the gap between buying a new property and selling an existing one. It provides quick access to funds when time is crucial, especially during sale delays.

Bridging Loans are commonly used for:

- Bridging the gap between buying and selling prop

What is a Bridging Loan?

A bridging loan is a short-term financing option that helps borrowers bridge the gap between buying a new property and selling an existing one. It provides quick access to funds when time is crucial, especially during sale delays.

Bridging Loans are commonly used for:

- Bridging the gap between buying and selling properties

- Temporary financing for investment maturation

- Funding urgent projects

- Quick access to capital

Bridging Loan Overview

Loan Amount:Loan Term:Interest Rate:Lenders£50K to £50M1 – 24 MonthsCustomized for Individual LoansWhole of Market

How does a bridging loan work?

Bridging loans are an excellent solution for filling a temporary financial gap. They come in handy when you need to borrow money for a short period. These sort of loans are ideal for time-sensitive transactions (auctions) or when you’re purchasing a new home but haven’t sold your current one yet.

Let’s take a closer look at how a typical bridging loan operates:

Step 1:

After spotting a house in an auction with great potential for refurbishment and subsequent profitable resale, you've set aside £75,000 to invest. However, it's important to note that the auction's reserve price is £250,000.

Step 2:

Your next step involves evaluating the property's renovation requirements, which are estimated to cost £100,000. Upon completion of the refurbishment, the property's value is expected to soar to £500,000.

Step 3:

At this stage, you have the option to approach a bridging company for assistance in acquiring the property and financing the renovation expenses.

Step 4:

After completing the renovation, you have two options: sell the property, settle the bridging company's debt, and keep the profit, or refinance the property, clear the bridging company's debt, and lease it for a monthly income.

Bridging Loan Example

1. Bridging Loan for Purchasing a New Property (Chain Break Bridge):

Tom has successfully exchanged contracts with the seller of his new property, but his purchaser's solicitor requires additional time to fulfil a mortgage condition. As the agreed-upon completion date for purchasing the vendor's property is rapidly approaching, Tom finds himself in an urgent situation. To fulfil his obligation to buy the new property while his current home is still on the market, Tom requires a bridging loan. The loan will be promptly repaid once his existing property is sold, resolving the temporary financial gap in the process.

2. Bridging Loan for Renovation (Renovation Bridge):

In the process of renovating a buy-to-let property, Joanne finds herself in need of additional funds to cover the renovation costs. To address this financial requirement, she decides to apply for a bridging loan.

Once the renovation work is completed, Joanne plans to repay the loan either by selling the property or by remortgaging it, ensuring a smooth resolution of her financial obligations.

3. Faster House Purchase (Auction Bridge):

After successfully purchasing a property at an auction, John faces the urgency of obtaining rapid financing. Traditional lenders are unable to process a mortgage within the necessary timeframe, leading him to choose a bridging loan as an alternative solution. Following the purchase, John plans to secure a long-term lender, allowing him to repay the bridging loan effectively and achieve a seamless financial transition.

4. Investor Cash Buyer (Drawdown Bridge):

Dawn aims to swiftly acquire investment properties but requires additional available cash. To address this, she establishes a pre-approved drawdown bridge, utilising the equity in her current properties. This enables her to promptly secure new properties without the delays associated with a traditional mortgage. Subsequently, Dawn can remortgage the acquired property, using the funds to repay the bridge loan, thereby preparing herself for future property purchases.

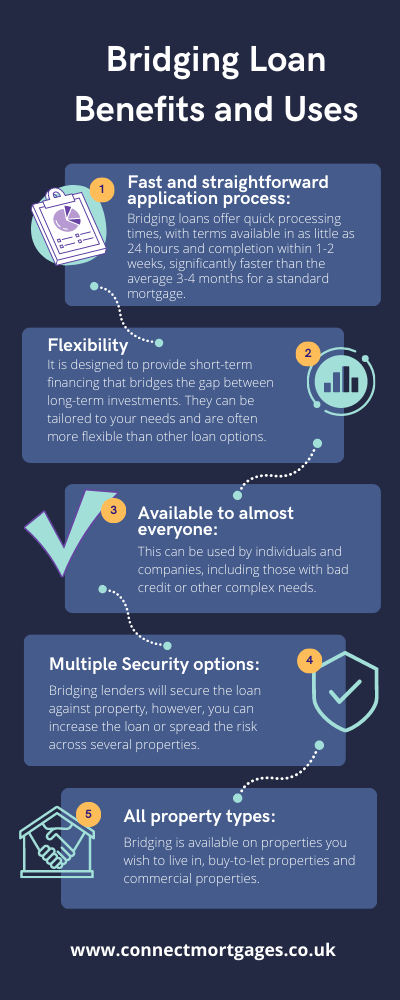

Bridging Loan Benefits and Uses

Discover the diverse benefits and versatile uses of bridging loans with our insightful infographic below:

Types of Bridging Loans

Bridging loans are short-term loans used to buy a property before selling or refinancing another one. They can be of two types: open or closed.

A. Open bridging loans

Open bridging loans: For buyers who need flexibility and speed. They can repay the loan when they want, but they pay higher interest rates and secure the loan with the property.

A. Closed bridging loans

Closed bridging loans: For buyers who have a fixed repayment date. They pay lower interest rates, but they need to provide proof of how they will repay the loan.

Alternatives to Bridging Loans

- A Personal Loan

- Secured Loan

- Business or Personal Overdraft

- Invoice Financing

- Asset Finance

- Credit Cards

Mortgage Advice..

Thinking of getting a mortgage? Our experienced team of skilled mortgage advisers are here to offer the essential guidance you require. Relying on our comprehensive understanding of the mortgage market, we’ll ensure you secure the perfect mortgage to suit your specific situation.

Pros and Cons of Bridging Loans

Both the pros and cons should be considered when considering whether a bridging loan is right for you.

Pros of Bridging LoansCons of Bridging LoansEasy to obtain and quick access to funds.Higher interest rates because of the high-risk nature.Underwriting considers various circumstances and property types.A repayment plan is required before approval.Short-term commitment to short-term plans.The potential need for refinancing or loan extension, resulting in additional cost.Flexible and tailored to meet borrowers’ needs.

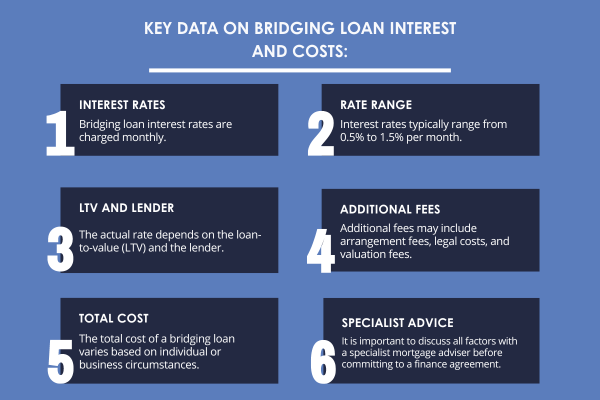

Bridging Loan Interest and Costs

Bridging loans can be invaluable in helping individuals or businesses reach their goals. However, they can be more expensive than other loans, so it is essential to understand the associated interest rates and fees before deciding. Bridging loan interest rates are charged monthly. They typically range from 0.5% to 1.5% per month, depending on the loan-to-value (LTV) and the lender.

Additional fees may include arrangement fees legal costs, and valuation fees. The exact cost of a bridging loan will depend on an individual’s or business’s specific circumstances. Therefore, discussing all factors with a specialist mortgage adviser before committing to any finance agreement is essential.

Final Thought

Bridging loans represent a valuable financing solution for both individuals and businesses seeking to fulfil their short-term financial requirements. They prove particularly useful in bridging the gap between financial transactions or obtaining quick access to funds. However, before committing to a loan agreement, it is crucial to comprehend the associated interest rates, fees, and repayment terms.

By following the steps outlined above, you should be able to secure a bridging loan that suits your purpose successfully. A bridging loan becomes a priceless asset in achieving financial success when sourced with the right lender and a clear understanding of the terms.

Our team of qualified mortgage advisers are available to address any inquiries you may have about bridging loans. We are here to assist you in making the most informed decision for your financial future. Why not contact us today to see how we may assist you?

FAQs: Bridging Loan

Most frequent questions and answers about bridging loan

How much does a bridging loan cost?

A bridging loan typically costs between 0.5% to 1.5% per month. Although the market has become quite competitive and, depending on the LTV, starts as low as 0.4% per month.

Other costs include valuation and legal fees. The lender will also charge an arrangement fee, typically 2% of the loan amount, which may be added to the loan or taken as a one-off payment.

How long does it take to get a bridging loan?

Bridge loans are quicker than traditional mortgages. Many bridge lenders offer very quick turnaround times, so it is possible to complete a loan in 1-2 weeks. However, because there is still a legal transaction to be completed, typically, the process will take 4-6 weeks.

Are bridging loans a good idea?

A bridging loan is a great solution for short-term financial needs or to bridge cash flow gaps. However, it is important to fully understand the costs of the loan before committing to it.

Are bridging loans expensive?

Bridging loans can appear to be expensive due to higher interest rates and arrangement fees associated with them. However, the cost becomes relative when compared with the missed opportunity if a bridging loan was not used. It is important to understand all costs before taking out a bridge loan.

Does a bridging loan affect a mortgage application?

Bridging loans are a short-term solution and should not have a long-term impact on mortgage applications.

Who can get a bridging loan?

Anyone who owns a property and needs short-term financing can apply for a bridging loan. The loan and interest rate will be dependent on your financial circumstances and the property.

Are bridging loans regulated by the FCA?

Some bridges are regulated by the Financial Conduct Authority (FCA) but only where they are secured on your own home, and the funds are not used for business purposes. Buy-to-let and commercial bridging loans are generally not regulated.

How much can I borrow with a bridging loan?

The amount that you can borrow through a bridging loan will depend on the value of your property and its current market value. Generally, you can borrow up to 75% of the market value of your property. You can achieve up to 100% bridging loan with additional property security.

What are the Uses of Bridging Loans?

Construction projects: They can fund construction projects, including new builds and land purchases with or without planning permission.

Expansions or renovations: Bridging loans can be used to extend, convert, or renovate any type of property.

Investments: They provide funding for investment projects involving properties that will be sold for profit.

Bridge the gap: They serve as a chain-breaking option, allowing the purchase of a new property while waiting for another to sell.

Unexpected expenses: Bridging loans can cover unexpected costs, like medical bills, tax bills, or urgent home repairs, provided there is a repayment plan within 12 months.

How to Exit a Bridging Loan?

Applying for a bridging loan is relatively straightforward, and a good specialist mortgage adviser will handle the process for you. However, before you apply, you can prepare your information to speed up the process.

To start applying for a bridging loan, gather all the necessary paperwork and documents. These might include bank statements, proof of income, tax returns, financial statements, and other evidence pertinent to your loan application.

A bridge lender will want to understand your financial position, but they will also place a great deal of importance on how you will pay the loan back before the end of the term. This is called the bridge exit route.

There are two main ways to exit a bridge. One is to sell the property. The other is to refinance the property onto a longer-term loan.

If you plan to sell the property or another related property to repay the bridge loan, the lender will assess the feasibility of this. For example, how long will it take to sell, anything you need to do to the property to make it sell, local demand etc.

If you plan to refinance the bridge loan onto a longer-term loan, again, the lender will check the feasibility, such as do your finances meet the lender’s criteria. They may ask you for confirmation from your adviser or refinance lender that you have an initial decision in principle from a lender to confirm this.

One risk is that markets or circumstances can change, and the plans for exiting the loan may no longer work. If you do not exit a bridge loan within the bridge loan term taken, there are usually substantial penalties.

A Connect, our advisers will help you to think through several exit routes to minimise this risk. They will also recommend reputable bridge loan funders that they can help you to negotiate an extension with should your plans take longer than expected.

Commercial Loan

Bridging Loan From £50K- £50M

Development Finance

Your search for commercial loan solutions ends here! Our guide helps you navigate the loan process. Consequently, you’ll find the perfect financing solution for your business. By reading this guide, you gain valuable insights into commercial loans. Furthermore, if you need more assistance, feel free to contact us. We’re here to help!

Wh

Your search for commercial loan solutions ends here! Our guide helps you navigate the loan process. Consequently, you’ll find the perfect financing solution for your business. By reading this guide, you gain valuable insights into commercial loans. Furthermore, if you need more assistance, feel free to contact us. We’re here to help!

What is a Commercial Loan?

A commercial loan is a type of loan specifically designed for businesses. It is typically used to purchase commercial property.

Additionally, it finances capital expenditures and funds other business operations. Moreover, it supports investments.

A commercial loan used for:

- Purchase commercial real estate

- Finance capital expenditures

- Fund business operations

- Fund investments

- Capital to support growth and expansion

Commercial Loan Overview

Loan AmountLoan TermInterest RateLenders£50K to £25M1 to 25 YearsCustomised for individual loansMultiple lenders

* Unsecured Commercial Loans, typically under £50K are also available

Advantages of a Commercial Loan or Mortgage

A commercial loan is a versatile option used for various purposes. For instance, it can help in buying commercial property, financing business expansions, or acquiring equipment. Moreover, these loans offer several advantages.

Lower interest rates

Commercial loans can have lower rates compared to other types of financing, helping businesses save on borrowing costs.

Bespoke underwriting

Commercial loans offer tailored terms based on financial circumstances and collateral, allowing for potential negotiation.

Extended terms

Commercial mortgages provide longer repayment periods, making them suitable for commercial property financing and allowing businesses to spread out costs.

Specialist lenders

Commercial loan specialists offer flexible terms, including interest-only options and higher borrowing amounts, beyond what traditional banks provide.

Flexible payment structures

Specialist commercial lenders may offer custom payment structures, such as initial interest-only periods, accommodating businesses' budgetary needs.

Types of Commercial Loan

Commercial loans are an essential source of financing for businesses, offering various options to meet their needs. From term commercial mortgages to asset financing, businesses can find suitable loan options. Let’s explore the different types briefly:

Commercial Term Mortgage:

A mortgage for property financing, either for business occupancy or investment.

Business Overdraft:

Flexible funding provided by the bank, usually requiring some security.

Start-up Loans:

Unsecured loans up to £100,000 offered to new businesses for their initial years.

Commercial Development Loan:

Used for purchasing or constructing commercial properties, with short-term structures.

Merchant Cash Advances:

Upfront funds provided in exchange for a portion of future credit/debit card sales.

Bridge Loans:

Short-term loans that bridge the gap between current and desired financial situations.

How to Apply for a Commercial Loan

The application process for a commercial loan depends on the type of loan, lender and borrower. There are four steps involved.

Previous slideNext slide

It is important to note that the process and timeframe for a commercial loan may vary depending on the type of loan, lender, and borrower. To ensure you receive your loan in a timely manner, it is recommended to work with an experienced commercial advisor who can guide you through the entire process.

Commercial Mortgage or Commercial Loan Quote

Commercial mortgages and commercial loans have customized interest rates based on individual financial circumstances and offered security. To determine borrowing capacity and monthly costs, it’s advisable to consult a specialist finance advisor with commercial market expertise.

The way you present your finances and business plans influences lender offers. Lenders also have preferences for specific commercial sectors. For instance, one may favor industrial units while another prefers dentist practices.

Kay Global Financial Services skilled commercial advisors can optimize your application presentation to secure favorable lending terms from commercial lenders. Our advisors possess industry qualifications, experience, and operate under FCA-regulated practices. Although most commercial mortgages are not FCA-regulated, our advisors maintain the same high standards.

Commercial Loan Interest Rates

Commercial loan interest rates are influenced by factors such as creditworthiness, loan type, duration, size, and economic conditions.

Rates vary based on the loan type, with secured commercial mortgages typically ranging from 5-10% and unsecured business loans carrying higher rates.

It’s important to compare options and consider associated fees like application, legal, valuation, arrangement, and advice fees. Checking your credit score before applying is crucial, as it affects the interest rate offered.

Commercial Loan Requirements

When applying for a commercial loan, businesses must meet certain requirements and provide specific documents. Here are the key points to consider:

- Financial Statements: Detailed income statements, balance sheets, and cash flow statements are necessary for the loan application

- Tax Returns: Most lenders require at least one year's worth of business tax returns.

- Credit History: Depending on the loan type, lenders may request personal or business credit history from owners.

- Collateral Proof: Lenders often ask for collateral, such as property or assets, to secure the loan.

- Business Plan: A well-written plan outlining how the loan will be utilized and benefit the business is important.

- Identity Verification: Each owner must provide proof of identity, such as a passport or driver's license.

- Additional Documentation: Other documents like business licenses or permits may be requested.

Final Thought

Commercial loans offer business owners and entrepreneurs a variety of unique advantages. They provide access to the capital necessary for expansion, improved cash flow, and greater financial security.

With competitive interest rates, flexible repayment terms, and a plethora of loan products available, it’s no wonder that commercial loans are becoming increasingly popular as a means of funding business operations.

If you have any specific questions about setting up a commercial loan, don’t hesitate to contact us. We’re happy to help.

How to get a commercial loan?

To get a commercial loan, you’ll need to have a good credit score and a viable business plan. You will also need to provide financial statements, tax returns, and other documents that demonstrate your ability to repay the loan. Once approved, you may be asked to provide collateral or personal guarantees for the loan.

How do commercial loans work?

Commercial loans are a form of business financing that allows companies to borrow money for a variety of purposes. These loans can be used to purchase equipment, finance property, or cover other large expenses needed to keep the business running smoothly.

When applying for commercial loans, businesses must provide detailed information about their current financial situation and plans for using the loan money. Lenders will also evaluate the business’s credit history and ability to repay before approving the loan.

Commercial loans typically offer higher interest rates than personal loans but can be a great way for businesses to access capital for short-term or long-term needs. The repayment terms of commercial loans vary by lender and are typically based on the size of the loan, the purpose of it, and the borrower’s creditworthiness.

Repayments on commercial loans are usually made in monthly instalments over a set period. Depending on the lender and type of commercial loan, businesses may also be required to provide collateral or other security for the loan.

This is to protect lenders from default in case the business is unable to make its repayment. Understanding the terms and conditions of commercial loans is an important part of making sure businesses can secure the financing they need.

Can you get a commercial loan on a residential property?

No, commercial loans typically cannot be used to purchase residential properties. These types of loans are intended for business use only. If you have a mixed-use property, e.g. if you run a business from your own home, a specialist residential lender may consider this if the commercial use is the smallest part of the overall usage.

How hard is it to get a commercial loan?

Generally, you’ll need good credit and a solid business plan to qualify for a commercial loan. You may also need to provide collateral or personal guarantees for the loan. A good commercial mortgage broker can assist you in making the process easier.

How do commercial loans work?

Commercial loans are a form of business financing that allows companies to borrow money for a variety of purposes. These loans can be used to purchase equipment, finance property, or cover other large expenses needed to keep the business running smoothly.

When applying for commercial loans, businesses must provide detailed information about their current financial situation and plans for using the loan money. Lenders will also evaluate the business’s credit history and ability to repay before approving the loan.

Commercial loans typically offer higher interest rates than personal loans but can be a great way for businesses to access capital for short-term or long-term needs. The repayment terms of commercial loans vary by lender and are typically based on the size of the loan, the purpose of it, and the borrower’s creditworthiness.

Repayments on commercial loans are usually made in monthly instalments over a set period. Depending on the lender and type of commercial loan, businesses may also be required to provide collateral or other security for the loan.

This is to protect lenders from default in case the business is unable to make its repayment. Understanding the terms and conditions of commercial loans is an important part of making sure businesses can secure the financing they need.

Can you get a commercial loan on a residential property?

No, commercial loans typically cannot be used to purchase residential properties. These types of loans are intended for business use only. If you have a mixed-use property, e.g. if you run a business from your own home, a specialist residential lender may consider this if the commercial use is the smallest part of the overall usage.

How hard is it to get a commercial loan?

Generally, you’ll need good credit and a solid business plan to qualify for a commercial loan. You may also need to provide collateral or personal guarantees for the loan. A good commercial mortgage broker can assist you in making the process easier.

Is interest on commercial property loans tax deductible?

Yes, interest paid on commercial property loans is generally tax deductible. However, you should check with your accountant or a tax professional to confirm your eligibility and how it will apply to your specific situation.

Can you get a 30-year commercial loan?

Yes, some lenders offer 30-year commercial loans. However, terms and conditions may vary depending on the lender and your creditworthiness.

Do we get tax benefit on commercial property loan?

Yes, you may be eligible for tax benefits with a commercial property loan. Interest payments on the loan may be tax deductible, and other types of deductions may also apply. Check with your accountant or a tax professional for more information about how this applies to your specific situation.

Development Finance

Bridging Loan From £50K- £50M

Development Finance

Property development is crucial for economic growth and long-term prosperity. Moreover, housing developments and infrastructure improvements benefit from development finance. This funding supports projects that create meaningful change for local communities and residents.

What is Development Finance

Development finance refers to loans and

Property development is crucial for economic growth and long-term prosperity. Moreover, housing developments and infrastructure improvements benefit from development finance. This funding supports projects that create meaningful change for local communities and residents.

What is Development Finance

Development finance refers to loans and grants used to aid property development.

Moreover, both public and private developments can create jobs and stimulate growth. They also increase access to markets and resources, reduce poverty, and improve living standards.

Development can take many forms, such as building new flats. It can also involve expanding a single property into a larger dwelling or creating a new housing estate.

The Role of Development Finance

Development finance plays an essential role by providing the funding needed for developments. Consequently, these promote economic growth and bring about long-term change for local communities.

Development finance offers access to capital for small businesses and entrepreneurs who need funding for smaller projects.

Through development finance, these individuals can fund their projects and contribute to their local economy’s development.

Who offers development finance?

The first step in accessing development finance is understanding the different sources available. For example, development finance is available for small and medium housebuilders through the Government via The Levelling Up Homebuilders Fund. The Fund supports smaller housebuilders who struggle to access finance through traditional bank lenders, with loans starting from £250,000.

There are many lenders in the market who offer development finance. This includes high-street banks and specialist lenders. Consider a mortgage broker if your business bank rejects your development finance application. They specialise in development finance and can help find alternative lenders. This is because high-street banks often have stricter criteria than specialist lenders.

Private investors and businesses may finance development projects in exchange for equity stakes.

Once you identify a source of finance, ensure the project meets all regulatory requirements. This includes proving financial viability and environmental sustainability. The lender will need to see the full development plans.

CASE STUDY:

“.. A Limited Company was looking for a facility of £1.3m to buy a plot of land and develop it into residential property. Whilst one lender offered a 7% rate it had a 1% of GDV (end value) as the fee. Whereas an alternative lender offered a 9% rate with a fee of 1% of the initial facility amount instead. The Gross Development Value (GDV) was £2,500,000. As this case study demonstrates, we look at a variety of options available and work with the client to get the suitable deal for their circumstances..“

How Does Development Finance Work?

In this section, we focus on development finance for private property investors. Typically, investors use a limited company as their business vehicle for development. However, if the development is for the investor’s residence, it is usually in their name. This type of project is commonly called a ‘self-build’.

A. The project:

Before a lender considers financing a development, they must understand every project detail. This includes the acquisition cost, such as the cost of the land to be built on and whether there is planning permission for the build. Additionally, what will actually be built, and how much will it cost? Finally, what will be the market value of the completed property? This end value is called the ‘Gross Development Value’ or GDV for short.

B. Funding stages:

With traditional mortgages, funding is fully released at the time of purchase. With a development loan, the funding is released in stages as the development progresses. The developer will be expected to have some money to purchase the land or start the first phase of development. Funds will then be released as each phase of the development is complete.

C. Exiting the development loan:

Development finance is usually a short-term loan to cover just the project’s building phase. Once the build is complete, the development finance is normally repaid by the sale of the property, or refinancing the loan to a longer-term mortgage. If the planned exit is the sale of the property, but the developer would like access to the equity that has been created, this is possible using a development exit bridge loan.

Mortgage Advice..

Thinking of getting a mortgage? Our experienced team of skilled mortgage advisers are here to offer the essential guidance you require. Relying on our comprehensive understanding of the mortgage market, we’ll ensure you secure the perfect mortgage to suit your specific situation.

Benefits of Development Finance

Development finance offers several key benefits for developers. Firstly, it provides an easy way to secure funds to purchase land or property and complete work. The loan is released in stages as each work stage is completed. This ensures developers have enough capital for larger projects without overstretching their budget.

The loan can be tailored to individual needs, allowing better cash flow management by releasing funds only when necessary. Furthermore, development finance often has a more flexible approach than traditional borrowing. This means developers can access capital even if they cannot meet strict requirements from banks and other lenders.

Consequently, it becomes easier for developers to access the funds they need to bring their projects to fruition. Development finance provides the necessary capital to complete tasks more quickly and with greater financial security.

Development finance may be perfect if you seek a financing solution tailored to your project’s needs. With quick access to capital and customised loan terms, you can ensure your project is completed on time and within budget.

Development Finance Lenders

Our development finance lenders offer long-term, short-term, and bridging loans to support various projects. Furthermore, our expert advisers can assist you in finding the most suitable lender for your needs. These range from small residential redevelopments to large-scale builds.

We have access to many lenders, including banks, specialist funds, and independent lenders. Thus, our lenders can provide the best development loan based on your project’s requirements. Additionally, our expert advisers will help you source the right funding.

Our advisor team also offers advice and assistance with structuring your deal. Moreover, they guide on the various tax implications that may apply. With Kay Global Financial services, finding the right finance for your project is easy.

We will help you find a lender that meets your needs and provide full support throughout the process. Get in touch today to discover how we can assist you with development finance.

Not only do we offer a wide range of products to cover your project’s needs, but the team at Kay global Financial Services also provides invaluable advice. Our assistance extends through every stage of your development finance journey.

The difference between development finance and other investment finance products

For certain projects, alternative finance, such as buy-to-let mortgages or standard bridge loans, may better suit your needs.

For example, if you are buying a ready-built property to renovate and make more attractive, a buy-to-let mortgage may be more suitable.

This will depend on the work planned and if the property, in its current condition, could still be let out. For instance, the property could be let out in its current condition.

However, you plan to add a new kitchen and bathroom and decorate throughout, which will take less than a few months. In this scenario, a buy-to-let mortgage is likely to be still suitable. Buy-to-let loans are cheaper than development loans and are already longer-term, so there’s no need to refinance once the work is complete.

If you plan to develop an existing ready-built property but can’t be let in its present condition due to the level of work needed, consider a bridge loan.

Bridge lenders are happy to lend on existing properties being developed, such as extensions or conversions. As long as the property remains watertight and does not require planning permission, then a bridge lender may be a suitable solution. Bridge loans are not cheaper than development loans, but they are more straightforward and quicker to arrange.

Development finance will always be required when a development project involves building from the ground up. Projects requiring planning permission or where an existing property won’t remain watertight are best served by development finance.

Working with a specialist mortgage broker, such as Kay Global Financial Services, can help you secure the right finance for your project. Our team of experts understands the complexities of sourcing funds for property developers.

Therefore, we can provide valuable advice on getting a suitable deal from lenders. We will help you identify appropriate lenders, negotiate ideal rates for your development project, and ensure all paperwork is completed promptly.

We understand that each development finance transaction has unique criteria, and our team is dedicated to finding the most suitable lender for every borrower.

We take an individual approach to each client’s situation, ensuring that you are fully supported throughout the process. By taking advantage of our experience and knowledge, we can help you get the development finance you need for your project.

Development Finance Market and Challenges

The development finance market has grown as lenders recognise the need for specialised services. Additionally, regional and local sources of capital are increasingly vital as more projects benefit from public and private investments.

Meanwhile, competition in the market is intensifying. Lenders now offer more competitive rates and terms, driven by the need to remain competitive in a growing market of borrowers seeking development finance.

Lenders face challenges when providing development finance. They must factor in potential risks when setting rates and developing products.

Lenders conduct extensive due diligence on prospective developments. This ensures that the borrower is qualified and has the resources to complete the project. Moreover, lenders must verify that the development will not harm local communities or businesses.

Lenders also face increasing pressure from government regulations and compliance requirements. These must be met for a loan to be approved. This means lenders need the necessary experience and understanding of relevant regulations before providing finance. Additionally, developers must have the appropriate planning permissions in place.

In summary, the development finance market is an ever-changing landscape. There is increasing competition and more demanding requirements for lenders. Therefore, lenders must assess their risk while complying with government regulations to succeed.

At kay global financial Services, we aim to save you time and money in sourcing development finance. We can advise on the ideal options available. We ensure the process runs smoothly and help you get the most competitive deal. To find out more, contact us today. We will be happy to discuss your requirements in detail.

Final Thought

Development finance is increasingly important and complex. However, by working with the right mortgage broker, such as Connect Mortgages, borrowers can get a suitable deal when sourcing funds for their project.

Our team of experts understand the complexities of this sector. Therefore, you can rest assured that you will receive the right advice and support throughout your development journey. If you are looking for a reliable mortgage broker to help with your project, look no further than Kay Global Financial Services.

Contact us today, and let us show you how we can help you get the development finance you need.

HOW TO GET FINANCE FOR PROPERTY DEVELOPMENT?

To get finance for property development, you can research the market and approach lenders directly. However, working with a reliable development mortgage broker, such as Kay Global financial Services, offers more benefits. Their advice covers many potential solutions, helping you find the most suitable lender for your project.

Our mortgage team of experts are knowledgeable in this sector. They provide expert advice and support throughout the entire process.

DO I NEED DEVELOPMENT FINANCE TO RENOVATE AN EXISTING PROPERTY?

You will not always need development finance to renovate a built property. Instead, a buy-to-let or bridge loan may be more suitable. This depends on the level of work and the property’s lettable condition.

HOW DO DEVELOPERS FINANCE PROJECTS?

Developers will need some initial funds to acquire the asset or start the first stage of development. Development funding can then be raised to fund each of the phases of the development until it is complete. The property can then be sold to repay the development loan, or refinanced to a term loan such as a buy-to-let.

WHAT TYPE OF INFORMATION DO LENDERS NEED FROM ME WHEN PROVIDING DEVELOPMENT FINANCE?

When providing development finance, lenders typically require a detailed business plan to assess the project’s viability. Additionally, they need evidence of the developer’s financial and experience credentials. They will want to understand the cost of the works.

Furthermore, they will assess the end value (GDV) of the project. Development finance lenders usually expect the applicant to have experience with developments. Alternatively, the applicant should work with a professional who has relevant experience.